Reeves Claims Britain Is “Fastest-Growing” in the G7 — The Numbers Don’t Stack Up

A closer look at growth, inflation, borrowing and jobs reveals a gap between the spin and the statistics.

This week we’ve had a run of major economic releases — and Rachel Reeves has been tweeting as if the numbers prove her “plan” is working. So let’s take her claims and compare them with what the latest data actually shows.

📊 Growth: however you measure it, the UK isn’t top

If you want the clearest barometer of economic performance, you start with the latest quarter — because that’s the freshest snapshot of what’s happening right now.

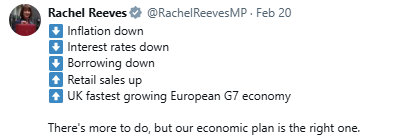

In the final quarter of 2025, the UK grew by 0.1%.

The United States grew by 0.4%.

Germany and Italy grew by 0.3%.

France grew by 0.2%.

So on the latest quarter, Britain is not leading the G7, or the European G7 — it’s sitting in the lower half of the table.

But let’s assume Reeves wasn’t talking about the latest quarter. Let’s assume she meant annual growth. Even then, the claim doesn’t stack up.

In 2025, the United States was the fastest-growing economy in the G7, not the UK.

But there’s an even more important point. Headline GDP can rise simply because the population rises. What really matters for living standards is GDP per head.

And on that measure, the UK economy has gone backwards — with GDP per person falling for consecutive quarters.

That means the economy might be ticking up slightly in aggregate terms, but on a per-person basis, Britain is getting poorer.

I broke that down in detail here:

So when Reeves says Britain is the “fastest-growing” economy, she’s not just stretching the G7 league table — she’s ignoring the fact that living standards per person are contracting.

That’s the number that actually matters.

📉 Inflation: Lower this month — but higher than when Labour took office

Reeves points to inflation being down, and again, that’s technically true month-to-month.

But the honest benchmark is where inflation stood when Labour took office.

In June 2024, inflation was 2.0%. The latest figure is 3.0%. So inflation is 1 percentage point higher than when Labour entered government — and still well above the Bank of England’s 2% target.

And there’s another key point: a big chunk of the improvement in the latest inflation reading is linked to transport, particularly fuel and travel-related costs. Those are heavily influenced by global oil prices and seasonal patterns — not something controlled by Rachel Reeves.

So yes, the number has moved in the right direction this month. But it’s still worse than the starting point Labour inherited — and much of the short-term movement reflects factors outside government policy.

🏦 Interest rates: Not set by Reeves — and countries move in step

Reeves also celebrates falling interest rates.

But interest rates are decided by the Bank of England, not the Chancellor. That independence matters — and it’s exactly why politicians shouldn’t claim credit for rate decisions.

It’s also worth understanding why many countries’ interest rates tend to move in the same direction around the same time.

Major economies are linked through global finance. If one big central bank cuts rates while others don’t, money flows can shift quickly, currencies can move, and that affects trade and inflation. So central banks watch each other closely — especially the United States — and rate cycles often happen broadly in step across countries.

So falling rates aren’t proof of a unique UK policy success. They’re a central bank decision, in a world where rate cycles are global — and Reeves doesn’t control them.

💷 Borrowing: a good month isn’t a plan

A January surplus makes a great headline — but January is always flattered by self-assessment receipts, and this year there are clear reasons to suspect the month was boosted by one-offs and timing effects.

Capital Gains Tax changes introduced from Autumn 2024, and then staged increases after that, created an obvious incentive for investors to bring forward disposals ahead of higher rates — a classic “forestalling” effect. When people sell earlier to lock in a lower rate, the cash still tends to show up later through self-assessment, which is why a big chunk of receipts land around January.

That doesn’t mean the public finances have suddenly been “fixed”. It means one month may have been flattered by behaviour that won’t repeat — and could leave a weaker picture later, including into the January 2027 self-assessment window.

So the government can celebrate a strong month if it wants. But it doesn’t change the underlying question: what’s the sustainable position when you strip out the one-offs?

👷 Jobs: the indicator Reeves didn’t mention

Another key economic indicator this week was the labour market — and unsurprisingly, given how weak it’s becoming, it’s the part Rachel Reeves didn’t even bother to mention.

Unemployment is now at a near five-year high, and the picture is especially grim for younger workers. Youth job losses are mounting, payroll employment is trending down, and the obvious risk is that opportunities dry up first for people at the start of their working lives.

That matters for the public finances too. A weaker jobs market doesn’t just hit families — it hits tax receipts and pushes up welfare spending. And when you raise the cost of hiring through Labour’s “jobs tax”, you make that problem worse, particularly for entry-level roles.

I broke down the youth jobs picture in full here:

🌍 Another story that caught my eye this week

And that brings me to another story that caught my eye this week — because it links directly to the same question: can you really claim you’re getting the public finances under control if you ignore major drivers of welfare spending?

The Centre for Migration Control says that over 18 months (January 2024 to June 2025), £10.6 billion of Universal Credit was paid to households containing at least one unemployed foreign national.

Universal Credit is paid at the household level, so it can include British family members too — and “unemployed” reflects DWP classifications rather than a simple claim that nobody in the home ever works. But even with those caveats, the scale is hard to ignore.

We’ve previously written on Stat of the Nation about the cost of the asylum system. This analysis adds another dimension: the ongoing welfare bill.

Because when borrowing is still high, and taxes are already heavy, you don’t get to wave around a January surplus and declare victory — not while major structural spending pressures are still running in the background.

✍️ Jamie Jenkins

Stats Jamie | Stats, Facts & Opinions

📢 Call to Action

If this helped cut through the noise, share it and subscribe free by entering your email in the box below and get the stats before the spin, straight to your inbox (no algorithms).

📚 If you found this useful, you might also want to read:

📲 Follow me here for more daily updates:

Great accurate analysis using the right numbers, Jamie. It would seem Rachel from accounts has been having lessons from Diane Abbott !