£24.3bn Borrowed In April — Spending Is Outrunning Labour’s Tax Rises

Labour raised taxes. But April’s figures show the state is spending even faster — with borrowing at £24.3bn and debt interest at a record April high.

The latest public sector finance figures are striking. According to the Office for National Statistics, the UK public sector borrowed £24.3bn in April 2026. That was £4.9bn higher than April 2025, a rise of 25.1%, and £3.4bn higher than the Office for Budget Responsibility had forecast.

That matters because April is the first month of the financial year. Before the year has even got going, borrowing is already overshooting the official forecast.

To be fair, borrowing over the financial year to March 2026 was lower than the year before. But that is not the same as fiscal health. Britain still borrowed £129.0bn last year, and April has now started the new financial year above forecast.

Labour has raised taxes. Employer National Insurance is bringing in more money. But the public finances are still under pressure.

That is the story.

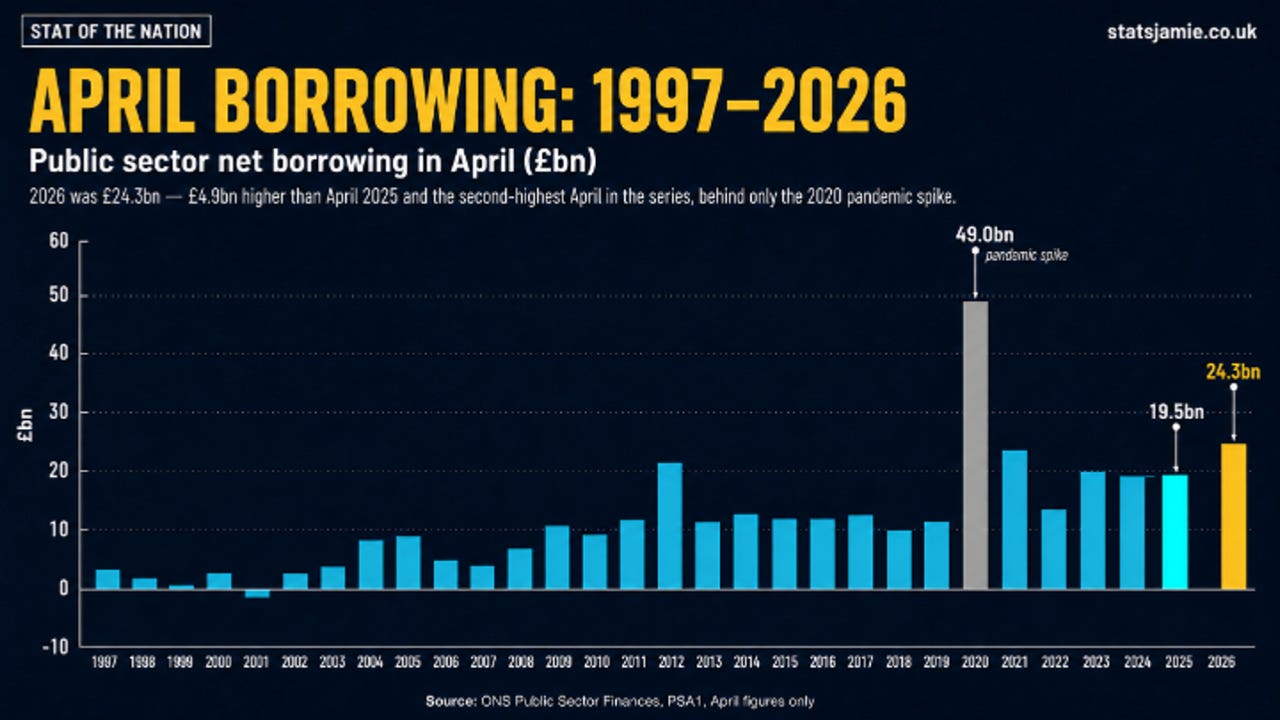

April Borrowing Is Historically High

The headline number is simple: the public sector borrowed £24.3bn in April 2026.

The ONS says this was the highest April borrowing figure since 2020, when the country was in the middle of the pandemic response. But the longer historical picture makes the point even more clearly.

Looking at April alone, going back to the start of the monthly series in 1997, April 2026 stands out as one of the largest April deficits on record. It is not as extreme as the pandemic spike in April 2020, when borrowing reached around £49bn, but it is still well above most of the pre-pandemic period.

That is what the chart below shows.

The reason for looking at April against previous Aprils is simple: monthly borrowing is seasonal. January often looks better because of self-assessed income tax receipts, while April has its own pattern. Comparing April with April gives a cleaner historical view than dropping one monthly number into the air.

And on that basis, April 2026 looks bad. Borrowing was £24.3bn, compared with £19.5bn in April 2025 — an increase of £4.9bn in a single year.

This is the bit Labour will not want to explain. They have already put up taxes. They have already hit employers with higher National Insurance. Yet borrowing is still going the wrong way at the start of the year.

Receipts Rose — But Spending Rose Faster

The key figure is not just the borrowing total. It is the gap between what came in and what went out.

Central government receipts were £85.5bn in April 2026, up £2.4bn on the year. Tax receipts alone rose by £1.8bn, including increases in income tax, corporation tax and VAT. Compulsory social contributions also rose to £15.4bn.

So this is not a simple story of the Treasury receiving less money. The Treasury received more.

The problem is that spending rose much faster. Central government current expenditure — the money spent on day-to-day activities — rose to £101.1bn, up £6.2bn on April 2025.

That is the public finance problem in one line:

Receipts up £2.4bn. Day-to-day spending up £6.2bn.

The state is taking in more. It is spending even more.

Benefits, Public Services And Debt Interest Drove The Increase

The rise in spending was not caused by one single item. It came from several familiar pressures across welfare, departmental spending and debt interest.

Net social benefits paid by central government increased by £2.7bn to £29.5bn, largely because many benefits are linked to inflation and State Pension payments are linked to earnings. Departmental spending on goods and services rose by £1.7bn to £38.8bn, with inflation pushing up the cost of providing public services. Debt interest also increased by £0.9bn to £10.3bn.

This is where the politics becomes difficult for Labour. They want to talk about investment, stability and fiscal responsibility. But the data shows a state whose running costs keep climbing.

Benefits are rising. Public service costs are rising. Debt interest is rising.

And taxpayers are being asked to keep feeding the machine.

Inflation Is Feeding The Debt Bill

The debt interest number deserves its own attention. Central government debt interest payable in April was £10.3bn, the highest April debt interest figure on record.

A major reason was the UK’s stock of index-linked gilts. These are government bonds where part of the cost moves with the Retail Prices Index. When RPI rises, the cost of servicing this part of the debt can rise too.

In April, the ONS said the RPI-linked “capital uplift” added £2.9bn to central government interest payable. That largely reflected a 0.4% increase in the RPI between January and February 2026.

That matters because inflation does not just hit families at the supermarket, the petrol pump or through higher bills. It also hits the government’s own debt bill. When inflation rises, parts of the national debt become more expensive to service — and when debt interest rises, taxpayers pay the bill.

This is the trap Britain is now in: high debt makes the country more exposed to inflation, and inflation makes the debt bill harder to control.

Rising Gilt Yields Could Make It Worse

There is a second pressure too: gilt yields.

A gilt is UK government debt. When the government borrows, it sells gilts to investors. The yield is the return investors demand for lending money to the UK. When gilt yields rise, the market is effectively saying: “we will still lend to Britain — but only at a higher price.”

I wrote recently about how Rachel Reeves spent months blaming Liz Truss for borrowing costs, only for gilt yields to surge under Labour as well.

That matters because higher yields do not just create bad headlines. They make future borrowing and refinancing more expensive.

The effect is not instant across the whole debt stock. Existing gilts are already issued at their original terms. But as old debt matures and the government issues new debt, higher yields mean the state has to borrow at higher rates.

That is the slow-burn danger. Today’s debt bill is being pushed up by inflation-linked gilts. Tomorrow’s debt bill could be pushed higher again if gilt yields remain elevated.

So the taxpayer gets squeezed twice: inflation pushes up index-linked debt costs today, while higher gilt yields make new borrowing and refinancing more expensive tomorrow.

That is why debt interest is not just an accounting detail. It is a warning light on the dashboard.

The Jobs Tax Has Not Fixed The Books

There is another important point buried in the financial year figures: Labour’s jobs tax is now showing up in the numbers.

Across the financial year ending March 2026, compulsory social contributions increased to £206.4bn, up £32.6bn, as changes to employer National Insurance contributions came into effect from 6 April 2025.

In plain English, the Treasury is taking in more money from employer National Insurance. But the public finances are still under pressure, and the jobs market is flashing red at the same time.

I wrote recently about how youth unemployment has hit an 11-year high and the early April PAYE estimate showed around 210,000 fewer payrolled employees over the year. That matters because higher employer National Insurance does not land in a spreadsheet. It lands in hiring decisions, vacancies, hours and entry-level jobs.

Borrowing for the financial year ending March 2026 was £129.0bn. That was down on the previous year, but it was still an enormous amount of borrowing. Then April opened the new financial year £3.4bn above forecast.

So the line is not complicated.

Labour taxed jobs, raised more money from employers, watched payroll employment fall by around 210,000 over the year, and still started April above the borrowing forecast.

That is not a clean bill of fiscal health. It is the cost of taxing work while the state keeps spending faster than the money comes in.

Debt Is Still Near 1960s Levels

The public sector balance sheet remains under pressure. Public sector net debt was estimated at 94.2% of GDP at the end of April 2026. That was 0.5 percentage points higher than April 2025, and the ONS says it remains at levels last seen in the early 1960s.

In cash terms, public sector net debt excluding public sector banks stood at around £2.943 trillion at the end of April. This is the long-term problem: Britain is carrying a huge debt burden, paying record April debt interest, and still borrowing heavily to cover day-to-day spending.

That is why the public finances feel permanently squeezed. It is also why every new promise from government now comes with the same question:

Who is paying?

Labour’s Fiscal Trap

Labour’s problem is not that the state has no money. The state is taking more.

The problem is that spending keeps rising faster than receipts. April’s numbers show it clearly: receipts rose by £2.4bn, day-to-day spending rose by £6.2bn, borrowing hit £24.3bn, debt interest hit £10.3bn, and debt remains near early-1960s levels.

This is the fiscal trap Britain is now in. Higher taxes have not created stability. Higher borrowing costs threaten future budgets. Inflation is feeding into the debt bill. And the taxpayer is still being handed the bill.

Conclusion

Labour promised economic stability. But the latest borrowing figures show something much less comfortable.

The government has raised taxes. Employer National Insurance is bringing in more money. Receipts are up. Yet borrowing has still started the financial year above forecast, debt interest has hit the highest April figure on record, and national debt remains near levels last seen in the early 1960s.

The state is not short of money. It is spending faster than taxpayers can fund it.

And when inflation feeds into index-linked gilts, and rising gilt yields threaten to push up future borrowing costs, the bill does not disappear. It lands on taxpayers.

That is Britain’s fiscal trap: higher taxes, higher spending, higher debt interest — and still more borrowing.

✍️ Jamie Jenkins

Stats Jamie | Stats, Facts & Opinions

📢 Call to Action

If this helped cut through the noise, share it and subscribe free by entering your email in the box below and get the stats before the spin, straight to your inbox (no algorithms).

📚 If you found this useful, you might also want to read:

Higher Interest Rates Won’t Fix Energy Shocks. They Just Hammer Households.

The Bank of England held interest rates at its latest meeting, but the real story was in the vote.

📲 Follow me here for more daily updates:

Do I need to order a wheelbarrow ? It’s all very worrying

The skint household keeps buying takeout and feeds the local rats!