Rachel Reeves Blamed Liz Truss — Now Borrowing Costs Are Surging Under Labour

Labour spent years blaming Liz Truss for Britain’s market credibility problem. But on 12 May, gilt yields surged — and voters should care because higher borrowing costs eventually land on taxpayers.

For years, Labour had one answer to every difficult economic question: Liz Truss.

Mortgage rates? Liz Truss.

Borrowing costs? Liz Truss.

Market credibility? Liz Truss.

But today’s gilt-market move should make Labour nervous.

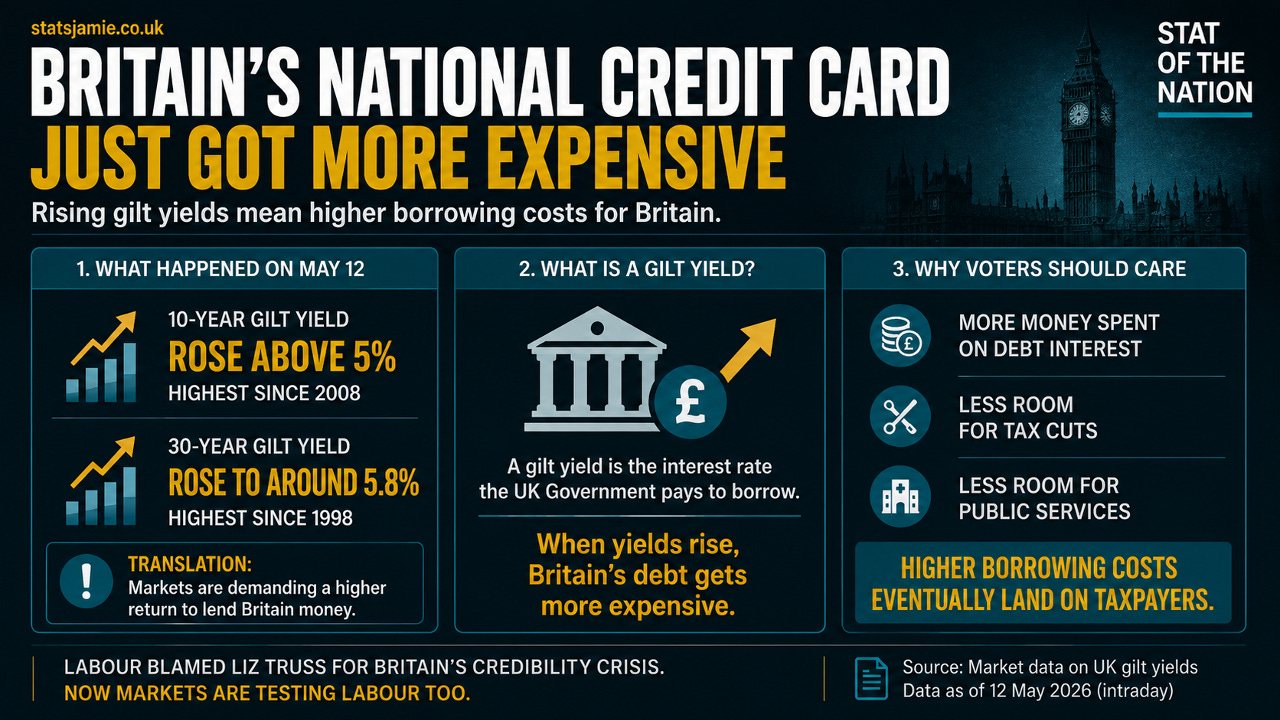

During a volatile trading session, the 10-year gilt yield moved above 5.1%, touching its highest level since 2008, while the 30-year gilt yield rose to around 5.8%, its highest level since 1998, before easing back slightly later in the day. Market data pointed to pressure from political instability, renewed inflation concerns and wider doubts over the UK’s fiscal position.

The numbers moved during trading. That is what markets do.

But the message was clear: investors were demanding a higher price to lend money to the UK Government.

The bond market does not care how many times Labour mentions Liz Truss.

It cares whether Britain’s numbers add up.

The Market Is Sending Labour a Warning

A gilt is UK Government debt.

When the Government spends more than it raises in tax, it has to borrow the difference. It does that by selling gilts to investors. The yield is the interest rate those investors demand for lending money to Britain.

So when gilt yields rise, the message from the market is simple:

“We will still lend to Britain — but only at a higher price.”

That is the warning now.

Investors are looking at the UK and seeing a dangerous mix: weak growth, high debt, sticky inflation, political instability and uncertainty over whether Rachel Reeves’ fiscal rules can survive Labour’s internal pressure.

This is not just about one leader or one Chancellor.

It is about whether the Government still has the authority to make hard choices — or whether Labour’s political panic ends with taxpayers funding another round of promises Britain cannot afford.

Why Should Voters Care About Gilt Yields?

Gilt yields sound boring.

They are not.

They are one of the clearest signals of how expensive Britain has become to finance.

In plain English, gilt yields are the interest rate on Britain’s national credit card. When they rise, the Government’s debt becomes more expensive. And that bill does not vanish into the financial system.

It lands on taxpayers.

The more the Government spends on debt interest, the less room it has for everything else: tax cuts, public services, defence, policing, infrastructure, or support for households.

If borrowing costs rise far enough, the Chancellor has only a few choices:

Raise taxes.

Cut spending.

Borrow even more.

Break the fiscal rules.

None of those choices are painless.

That is why voters should care. Gilt yields are not just a market statistic. They are a real-world pressure gauge on the public finances.

And because government bonds sit at the heart of the financial system, higher gilt yields can also feed into wider borrowing costs, including mortgages, business loans and other forms of credit.

So the question is not:

“Why should ordinary people care about gilts?”

The question is:

“Why should ordinary people ignore the interest rate on Britain’s national credit card?”

Why the 30-Year Gilt Matters

The 30-year gilt is especially important because it reflects long-term confidence.

This is not just about what the Bank of England might do next month.

It is about what investors think Britain will look like decades from now: how much debt it will carry, how much inflation it will tolerate, and whether politicians will keep control of the public finances.

When long-term borrowing costs rise, markets are not just reacting to today’s headlines.

They are asking whether Britain’s future finances are credible.

That should worry any Government.

What Labour Will Say

Labour will say this is about global markets, oil prices, inflation expectations and wider international uncertainty.

There is some truth in that.

Political turmoil is not the only factor pushing up UK borrowing costs. Inflation concerns, global bond-market pressure and wider uncertainty also matter.

But there was also some truth in that during the Truss episode.

Global conditions mattered then too. Inflation was high. Interest rates were rising. Bond markets around the world were under pressure.

Yet Labour still turned the gilt-market reaction into a simple political attack: Liz Truss crashed the economy.

So Labour cannot have it both ways.

If every rise in borrowing costs under the Conservatives was proof of Tory recklessness, Labour cannot now pretend that rising borrowing costs under Labour are just an act of God.

The question is not whether global markets exist.

The question is whether the UK is being punished harder because investors doubt the Government’s fiscal credibility.

That is the uncomfortable part for Labour.

The Causes Are Different. The Lesson Is the Same.

To be clear, this is not identical to the Liz Truss mini-budget.

The Truss episode was a sudden fiscal shock.

In September 2022, Kwasi Kwarteng announced major tax cuts without the normal full Office for Budget Responsibility forecast. The House of Commons Library later summarised that the mini-budget included tax cuts that would have reduced Treasury revenues by around £45 billion in 2026/27.

The market reaction was severe. On 28 September 2022, the Bank of England announced temporary purchases of long-dated UK government bonds to “restore orderly market conditions.”

So no, today is not the same event.

There has not been one dramatic mini-budget moment. There has not been an emergency Bank of England intervention on the same scale. And we should be honest about that.

But Labour’s problem is still serious.

It is not one Friday morning statement. It is a slower build-up of doubts: weak growth, high debt, rising debt-interest costs, political instability and concern that the fiscal rules may not survive pressure from within the party.

Truss lost market credibility in days.

Labour is now discovering that credibility can also drain away slowly — one weak forecast, one leadership wobble, one fiscal doubt at a time.

The causes are different.

The lesson is the same.

Markets punish governments when they think the numbers do not add up.

Labour’s Liz Truss Problem

This is where the politics becomes awkward.

Labour spent years using Liz Truss as the permanent explanation for Britain’s economic pain.

But if Labour keeps saying “Liz Truss crashed the economy”, voters are entitled to ask why borrowing costs are now surging under Labour.

If the answer is “global markets”, then Labour has to admit that not everything in 2022 was simply about Liz Truss.

If the answer is “political instability”, then Labour has to admit that its own internal chaos now has a real economic cost.

And if the answer is “markets are worried about borrowing and spending”, then Labour has to admit the central point:

Britain has a fiscal credibility problem.

Not just a Liz Truss problem.

A Britain problem.

The Real Cost Falls on Taxpayers

The danger with rising gilt yields is that they squeeze the Government from every direction.

A higher debt-interest bill means more taxpayer money going to bondholders rather than public services. It means less room for tax cuts. It means more pressure on the Chancellor to find savings. It makes every Budget more difficult.

This matters even more when Britain is already carrying a huge debt burden.

The more debt you have, the more exposed you become to higher interest rates. A country with low debt can absorb higher borrowing costs more easily. A country with high debt has far less room for error.

That is Britain’s problem.

When borrowing costs rise, the Government cannot simply pretend nothing has happened. The bill gets bigger. The choices get harder. The room for political fantasy gets smaller.

Higher gilt yields are not just numbers on a trading screen.

They are a warning that Britain’s public finances are becoming harder to sustain.

Conclusion: The Market Has No Patience for Spin

Labour spent years telling voters that Liz Truss proved the importance of market credibility.

They were right.

But credibility is not owned by one party. It has to be earned every day.

The bond market does not care how often Rachel Reeves says “stability”. It does not give Labour a discount because it spent years attacking Liz Truss. It looks at debt, borrowing, inflation, growth and political risk — then it sets the price.

Today, that price is rising.

And when Britain’s national credit card gets more expensive, taxpayers pick up the tab.

Labour wanted to make Liz Truss the symbol of economic chaos.

But the market is now sending Labour a message it cannot spin away:

The Liz Truss excuse is wearing thin. Britain’s debt problem is still here. And taxpayers are still the ones left carrying the bill.

✍️ Jamie Jenkins

Stats Jamie | Stats, Facts & Opinions

📢 Call to Action

If this helped cut through the noise, share it and subscribe free by entering your email in the box below and get the stats before the spin, straight to your inbox (no algorithms).

📚 If you found this useful, you might also want to read:

625,000 UK Resident Visits To Pakistan — So Why Is It Britain’s Top Asylum Source?

If Pakistan is so dangerous that it is Britain’s top source of asylum claims, then common sense says very few people would want to visit it.

📲 Follow me here for more daily updates:

Labour blame Brexit as well - for anything.

During the Liz Truss thing there was a problem with pension funds which I didn't quite understand. It was something to do with the value of Gilts falling and funds having to sell off assets to pay their obligations. The BOE had to step in. But Gilt yields are up higher now than they were then but we haven't heard anything about problems with pensions this time.

Very interesting article and very timely too, Jamie.

I was in conversation with a mate of mine at the weekend who was complaining about the cost on remortgaging his buy to let. He was blaming it all on Truss ( he is a lefty) and I tried to explain that as damaging as her budget was at the time, it was in reality little more than an aberration ie given all the economic and geopolitical events that have occurred in recent years . People seem to remember the turmoil unleashed on the bond market in the immediate aftermath of the Truss budget but most forget that within a matter of days ( after the B of E intervened) order was largely restored