The OBR’s Warning - Britain’s Tax & Spend Time Bomb

The Office for Budget Responsibility has delivered a warning Westminster cannot keep dodging.

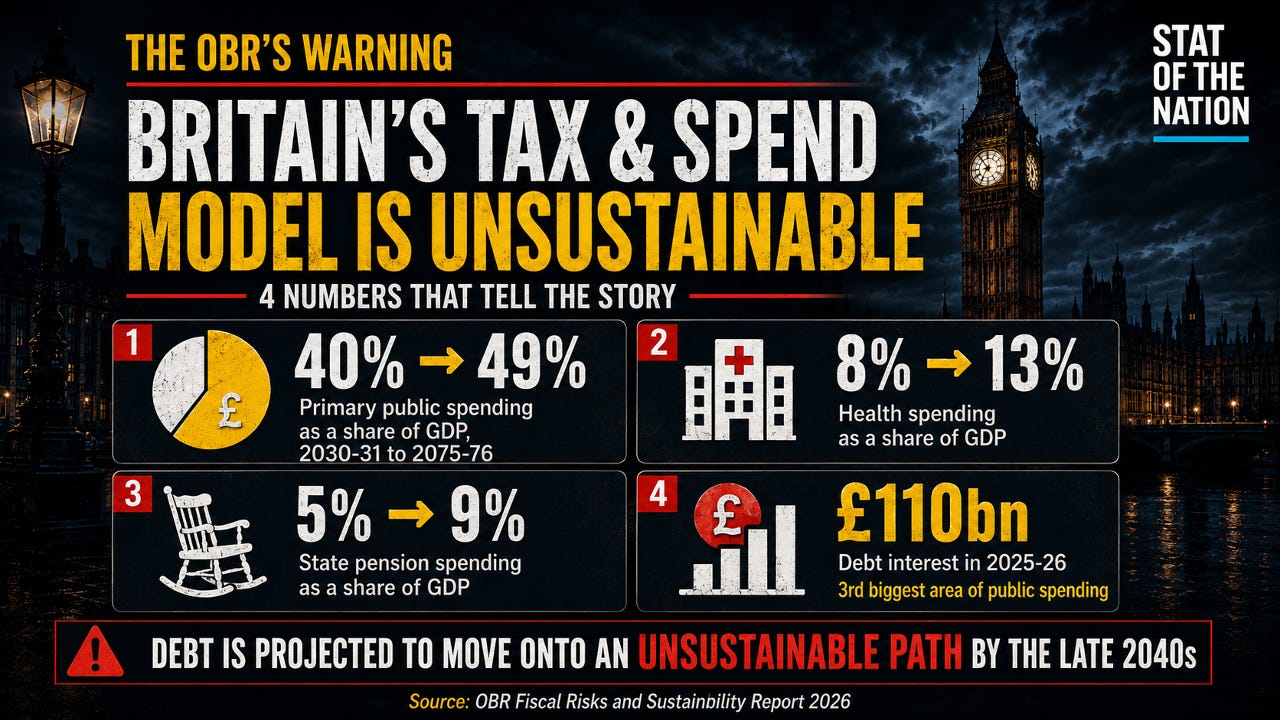

Britain’s current tax-and-spend model is not sustainable.

That is not a slogan from an opposition party or a newspaper headline. It is the conclusion of the independent body Parliament created to test whether government plans add up.

The warning should not come as a surprise. Borrowing is already running above forecast, debt-interest bills are rising and the tax burden is heading towards post-war highs. In the first two months of this financial year, borrowing reached £46.3 billion — £7.7 billion above the OBR forecast and £8.9 billion higher than the same point last year. May’s debt-interest bill alone was £11.7 billion, the highest for any May on record.

The OBR’s new report is the long-term version of the same problem.

Under current policy settings, almost every scenario it models sees UK debt move onto an unsustainable path.

That does not mean Britain is bankrupt today. It means future governments will eventually be forced into choices that today’s politicians keep avoiding: higher taxes, lower spending elsewhere, later retirement, reformed public services, or some combination of all four.

The longer they wait, the nastier those choices become.

We Are Starting From A Weaker Position Than Most Countries

The UK is not approaching these pressures with low debt and plenty of room to manoeuvre.

The OBR says the UK has experienced one of the largest increases in government debt, as a share of GDP, of any advanced economy over the past two decades. On an internationally comparable basis, UK debt has nearly tripled relative to the size of the economy since 2005.

In 2005, UK debt was close to the advanced-economy average. By 2025, it was 45 percentage points higher.

Against the G7 average, the UK went from being 23 percentage points below in 2005 to 6 points above in 2025.

The UK is entering an ageing era already carrying more debt, paying more interest and with less room to absorb the next shock.

Debt-interest spending has more than doubled as a share of GDP since before the pandemic. At £110 billion in 2025-26, it is now the third-largest area of public spending after health and welfare.

A quick note on the numbers: GDP is the total value of everything the UK economy produces in a year — the country’s overall economic output.

We measure debt, tax and spending as a share of GDP because a £100 billion bill means something very different for a £2 trillion economy than it does for a £5 trillion one. It shows how much of the country’s total economic capacity the state is taking up, and whether the bill is growing faster than the economy that must pay it.

The State Is Growing Faster Than The Economy Can Fund It

The OBR’s baseline scenario starts with public debt stabilising at just under 100% of GDP around 2030-31 — in other words, roughly equal to the value of the entire UK economy in a year.

But from there, the pressure builds.

Primary public spending, excluding debt interest, rises from around 40% of GDP in 2030-31 to almost 49% by 2075-76. Tax receipts remain broadly flat at around 41% of GDP.

That gap is the whole story.

Under current policy assumptions, the UK is projected to maintain commitments that the economy cannot sustainably finance. The primary deficit returns in the 2030s and eventually reaches around 7% of GDP. Add rising debt-interest costs and public sector net debt moves onto an unsustainable path by the late 2040s.

Debt interest alone could eventually reach 12% of GDP.

That means more of the money raised from taxpayers goes towards paying for yesterday’s borrowing, rather than schools, policing, defence, infrastructure or lower taxes.

Health, Pensions And Social Care Are The Main Bill

This is not a fiscal problem created by a few pointless Whitehall schemes.

The biggest pressures are the things people care about most: healthcare, pensions and social care.

By 2075-76, the OBR projects:

Health spending rising from around 8% of GDP to 13%.

State pension spending rising from 5% to around 9% of GDP.

Adult social-care spending rising from 1.2% to 1.8% of GDP.

Defence spending reaching 3.5% of GDP.

Older people are not the problem. People who have worked, paid taxes and National Insurance throughout their lives deserve dignity, healthcare and financial security in retirement.

The problem is that governments have made commitments without being straight about the long-term bill.

Much of the public-sector pension system is unfunded. Unlike a private pension scheme, there is no investment pot built up to meet the full future cost of pensions already promised. Future payments are instead a claim on future taxpayers.

That is not a criticism of public-sector workers. They are entitled to the pensions they were promised.

It is a warning about who ultimately carries the risk: future taxpayers.

Net Zero Is Another Cost The UK Government Has Chosen To Add

The OBR’s baseline is not only about health, pensions and social care.

It also includes the cost of the UK Government’s legally binding commitment to reach net zero by 2050.

The OBR estimates that public-sector investment supporting that transition totals £257 billion between now and 2050, in 2025 prices. That is the Government’s assumed share of a wider £720 billion of economy-wide investment.

At the same time, the transition erodes one of the Treasury’s most dependable tax streams.

The OBR projects net-zero-affected receipts falling from 1.6% of GDP in 2030-31 to 0.5% by 2075-76, largely because fuel-duty revenue is expected to collapse as petrol and diesel vehicles disappear.

As fuel duty declines, the Government is already looking for alternative ways to tax driving.

From April 2028, ministers plan to introduce Electric Vehicle Excise Duty: effectively a mileage charge for electric and plug-in hybrid cars, paid alongside existing Vehicle Excise Duty. The proposed rate is 3p per mile for fully electric cars and 1.5p per mile for plug-in hybrids.

The tax burden on driving is not disappearing. It is being redesigned.

So the Treasury faces two pressures at once:

More public investment to deliver the policy.

Less revenue from fuel duty, requiring new ways to tax motorists.

But it is another major commitment being added while debt is already high, taxes are rising and growth is weak.

The question ministers should answer is simple:

Who pays, how much, and what gets cut or taxed more when the bill arrives?

The Private Sector Cannot Carry Everything

The fundamental point is simple.

When I say the productive economy, I mean the private sector: businesses that employ people, invest, export, innovate and generate the profits, wages and taxes that fund the state.

The money government spends does not appear from nowhere. It comes from businesses making profits, workers earning wages and consumers spending money — or it is borrowed from future taxpayers.

Public services matter. A healthy, educated and secure country needs them.

But every public-sector salary, pension contribution, benefit payment and departmental budget must ultimately be paid for by taxes raised from the private economy, borrowing against future taxes, or stronger growth.

And that private-sector base is under pressure.

When employers face higher labour costs, workers lose more of each pay rise to tax, and investment is delayed, the part of the economy that pays for the state becomes weaker.

The OBR forecasts the tax-to-GDP ratio rising from 37% in 2019-20 to 43% by 2030-31.

Yet rising taxes have not removed the borrowing problem.

That tells us something important.

The issue is not simply that the state has too little money. It is that the state is trying to do too much with an economy that is not growing strongly enough to carry it.

Delay Is The Most Expensive Choice

This is the most important part of the OBR’s report.

To keep debt at roughly 95% of GDP by the end of the projection period, the OBR estimates that the UK would need a permanent fiscal tightening worth 3.8% of GDP from 2031-32 onwards.

That is roughly equivalent to total onshore corporation-tax receipts or the entire education budget in 2030-31.

And that is the cost of acting early.

If action is phased in gradually, the required adjustment rises to around 7% of GDP in the final decade of the projection. If action is delayed until the early 2050s, it reaches around 8% of GDP.

Every political party likes to imply that difficult decisions can be handled later.

The OBR has shown that “later” is not the gentle option.

It is the option that forces bigger tax rises, deeper cuts or harsher reforms onto the next generation.

The Choice Britain Keeps Avoiding

There is no painless answer.

Britain needs faster productivity growth. It needs a welfare and tax system that rewards work. It needs a serious plan for NHS productivity and social care rather than assuming spending can rise forever faster than the economy.

It also needs honesty about pensions, debt and the cost of the commitments governments keep adding.

The OBR has not said Britain is bankrupt today.

It has said the current model is not sustainable.

We cannot keep promising more, taxing more, borrowing more and hoping weak growth will somehow carry the bill.

Reform now is difficult. But leaving it to the next generation will be harder, more expensive and far more unfair.

The numbers do not care about the next election.

And eventually, neither will the markets.

✍️ Jamie Jenkins

Stats Jamie | Stats, Facts & Opinions

📢 Call to Action

If this helped cut through the noise, share it and subscribe free by entering your email in the box below and get the stats before the spin, straight to your inbox (no algorithms).

📚 If you found this useful, you might also want to read:

The Asylum Hotels Are Closing — But Is The Crisis Moving Onto Your Street?

In his speech this week, Keir Starmer listed falling small-boat crossings and closing asylum hotels among his Government’s achievements. He has also repeatedly promised to smash the criminal gangs behind the Channel crossings.

📲 Follow me here for more daily updates:

"Britain’s current tax-and-spend model is not sustainable." There is no tax and spend model, there's only a spend then tax model. Where would money, Govt IOUs, I Promise to Pay the Bearer, signed by the Chief Cashier of the BoE, originate if nor Govt? What comes out of the OBR ignores reality and so is demonstrable gibberish.

"The money government spends does not appear from nowhere." Yes it does. The process is called ex nihilo. Govt budgets then passes a Supply/Appropriation Bill (look them up in Hansard) forcing the BoE, part of Govt, under the 1866 Exchequer/Audit Act (Google is your friend here!) to create, as a loan, the money. Govt is self-funding. So money for defence? Welfare? Not a problem so long as the actual necessary resources are available.