Higher Interest Rates Won’t Fix Energy Shocks. They Just Hammer Households.

The Bank of England held rates at 3.75%, but one MPC member wanted a rise. If inflation is driven by energy and fuel costs, squeezing households harder won’t fix the cause.

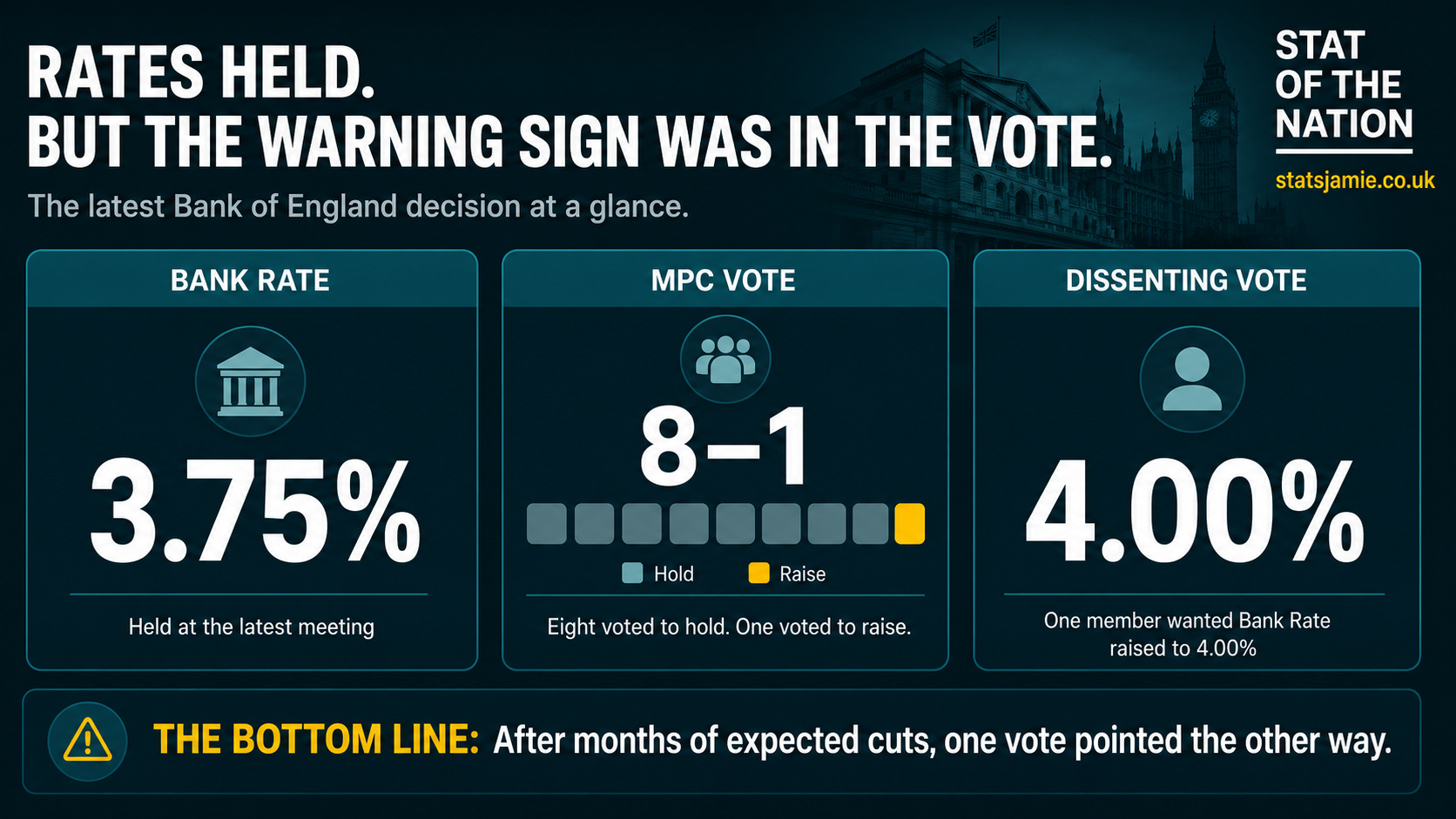

The Bank of England held interest rates at its latest meeting, but the real story was in the vote.

At its meeting ending 29 April 2026, the Monetary Policy Committee voted 8–1 to keep Bank Rate at 3.75%. One member wanted to increase rates by 0.25 percentage points, taking Bank Rate to 4%. After months of assuming rates were on the way down, Britain is now back in a world where some at the Bank are already thinking about pushing them higher.

The Bank’s concern is that inflation could prove more persistent, especially if higher energy costs feed into wages, prices and expectations. That is why the vote matters. One member of the MPC did not think holding rates was enough.

But if inflation is being driven by energy prices, fuel prices, imported costs and global shocks, hiking interest rates does not solve the cause.

It just makes households poorer.

The Warning Sign Was In The Vote

The headline is simple: rates stayed at 3.75%. But the split matters, because an 8–1 vote with one member voting for a rise tells us the Bank’s inflation reflex is still alive.

When inflation rises, the instinct is to squeeze demand. That makes sense if households are flush with money, borrowing cheaply, spending heavily and bidding up prices because too much money is chasing too few goods. In that world, higher rates cool demand, make borrowing more expensive, encourage saving and slow the economy.

But that is not the same as an energy shock. Higher interest rates do not refine more petrol, produce more gas or make food production cheaper. They do not solve the source of the inflation. They squeeze the people already paying it.

This Is Not Demand-Led Inflation

Not all inflation is the same.

There is a world where inflation is caused by excess consumer demand. People have too much spending power, firms cannot keep up, and prices rise. But the inflation shocks Britain has faced in recent years were not simply caused by households living the high life.

Families were not bidding up gas prices because they felt rich. Drivers were not pushing up diesel prices because they had too much disposable income. Parents were not demanding higher food bills.

They were being forced to pay more for essentials.

And when essentials go up, demand often falls elsewhere. If a household has to spend hundreds or thousands more on energy, fuel and food, it has less money left for restaurants, clothes, holidays, home improvements, subscriptions, local businesses and the high street.

That is not an overheated consumer boom. That is a cost-of-living squeeze.

So the question is obvious: why is the consumer punished as if they caused the problem?

The Second-Round Effects Argument

The Bank of England would argue that higher rates are not just about the original energy shock. Its concern is what happens next.

The theory is that energy prices rise, headline inflation rises, workers seek higher wages to protect their living standards, and businesses then raise prices to cover higher wage and input costs. That is what economists call second-round effects.

But look at what that means in practice.

If energy bills rise and workers ask for higher pay so they are not made poorer, the Bank sees that as a risk. If firms try to pass on higher input costs, the Bank sees that as a risk too. So the response is to weaken demand, cool the labour market and make it harder for wages and prices to adjust.

In plain English, the Bank is not reversing the original inflation shock. It is trying to stop people from catching up with it.

Higher rates do not produce more gas. They do not refine more petrol. They do not reduce food production costs. They do not lower the energy bills that started the squeeze.

What they do is make borrowing more expensive, reduce disposable income, weaken workers’ bargaining power and put pressure on businesses that were not responsible for the original shock.

That is the problem.

The Bank talks about preventing inflation becoming embedded. But for households, the experience is different: prices rise first, then mortgages rise, loans rise, rents rise, and people are told this is the medicine.

At some point, we need to ask a simple question.

Why should ordinary households be made poorer today because policymakers fear they might try to recover their living standards tomorrow?

What Happened Last Time

We have already lived through this.

UK inflation peaked at 11.1% in October 2022. The Office for National Statistics said the main drivers included energy, fuel and food prices, while the largest upward contributions came from housing and household services, including electricity, gas and other fuels, along with food and transport.

Typical household energy bills rose by 54% in April 2022, then by a further 27% in October 2022. Lower wholesale prices later helped bring bills down, but they remained well above winter 2021/22 levels.

That was the first hit. Then came the second.

The Bank of England raised interest rates sharply from near-zero levels, eventually taking Bank Rate to 5.25% in August 2023 before later cuts. Bank Rate influences borrowing costs across the economy, including mortgages, loans and credit.

That fed through into mortgage costs. People coming off cheap fixed-rate deals refinanced at much higher rates, households on variable-rate mortgages felt the pain more quickly, and landlords with mortgages faced higher costs too. Some of that pressure inevitably fed into rents.

So ordinary people were squeezed from both sides. First came higher energy bills, higher food bills and higher fuel costs. Then came higher borrowing costs and higher rents.

That is the double hit.

The Competence Question

Some second-round effects are not neatly stopped by raising rates. If benefits, pensions, contracts, rents, fares or other payments are linked to inflation, then once the inflation figure has happened, some later increases are already baked into the system. Higher interest rates cannot go back in time and erase the inflation reading.

This is why the timing matters. Inflation rises first, then interest rates rise, then mortgages and borrowing costs rise, and then inflation-linked payments may rise later. Households are still poorer anyway.

The Bank operates within global constraints. Britain imports energy, food, goods, raw materials and components. The exchange rate matters because a weaker pound can make imports more expensive, feeding back into inflation. The Federal Reserve does not set UK interest rates, but US monetary policy influences global markets, capital flows, bond yields, exchange rates and financial conditions.

So yes, the Bank does not control the global monetary weather.

But that does not absolve it of judgement.

Back in 2022, former Bank of England Governor Lord Mervyn King challenged the role central banks played during the Covid period. His argument was that lockdowns reduced the supply of goods and services, while central banks increased the supply of money. That created the classic inflation risk: too much money chasing too few goods.

That does not mean the Bank is causing inflation now. It means its recent judgement should not simply be waved through without challenge. The same institution that helped preside over the Covid-era monetary response then pushed rates up sharply after an energy shock. Now, with inflation risks returning, households are being asked once again to trust that higher borrowing costs are the right medicine.

Andrew Bailey was Governor during the Covid period and remains Governor today. He began his term on 16 March 2020, and remains in post.

If central banks helped fuel inflation after Covid, then responded to an energy shock by hammering borrowers, people are entitled to ask a simple question: how much confidence should we have in the institution prescribing the cure?

This is not just a technical debate.

It is a question of competence.

The Bigger Question

The Bank of England has a target. It wants inflation at 2%. But the public has a different concern.

They want to know why the response to higher energy bills is higher mortgage costs. They want to know why families are squeezed again because of a shock they did not cause.

If inflation is driven by excess demand, interest rates have a role. But if inflation is driven by energy shocks, fuel prices, imported costs and global instability, then higher rates are a blunt weapon.

They do not fix the source of the inflation. They spread the pain.

And the latest MPC vote shows the danger has not gone away. One member already wanted rates higher. The direction of travel may have changed.

Households could be about to discover, once again, that when inflation returns, the Bank’s first instinct is not to protect the consumer.

It is to squeeze them.

✍️ Jamie Jenkins

Stats Jamie | Stats, Facts & Opinions

📢 Call to Action

If this helped cut through the noise, share it and subscribe free by entering your email in the box below and get the stats before the spin, straight to your inbox (no algorithms).

📚 If you found this useful, you might also want to read:

The Two-Child Benefit Cap Is Scrapped And Taxpayers Pick Up The Bill

This week, as we moved into the new tax year, the two‑child limit in Universal Credit and Child Tax Credit was scrapped. Support is now paid for every child — not just the first two.

📲 Follow me here for more daily updates:

My illiterate questions are always "why does inflation need to be kept at 2%? Why not 4% or 1.5%? Wouldn't it find it's own position if the Bank stopped fiddling with interest rates? Why aren't there two interest rates - one for savers and one for borrowers? Why aren't mortgages on fixed for 25 year rates like they used to be?"

Questions, questions

Fair point though missed biggest real world pressure on finances which are house prices which have been 2x’d by qe and artificially low interest rates. Growth would always be theoretically better with lower rates. The qe thumb is still on the scale - depressing still interest rates. House prices are strangling growth. So whilst you can target growth without the conditions for long term sustainable growth ie 3/4x house prices you are pissing in the wind - which is what the last 17 years of qe have shown. We may face a road runner moment soon when the market looks at uk and says no way and we see gilts up at the 9% level…