Borrowing Surges — Would Burnham Make It Worse?

Markets are watching Labour’s spending instincts — and the numbers are already flashing red.

Markets do not vote in by-elections. But they do react to what those by-elections mean.

After Andy Burnham’s victory in the Makerfield by-election, The Telegraph reported that the cost of UK government borrowing rose at the fastest pace in Europe. The yield on 10-year gilts climbed from 4.76% to 4.82%, while the pound fell below $1.32 for the first time since April.

It would be too neat to put all of that on one by-election result. Markets may have been reacting to two things at once: the political risk of Burnham’s return to Westminster, and the fiscal reality of borrowing figures released the same morning.

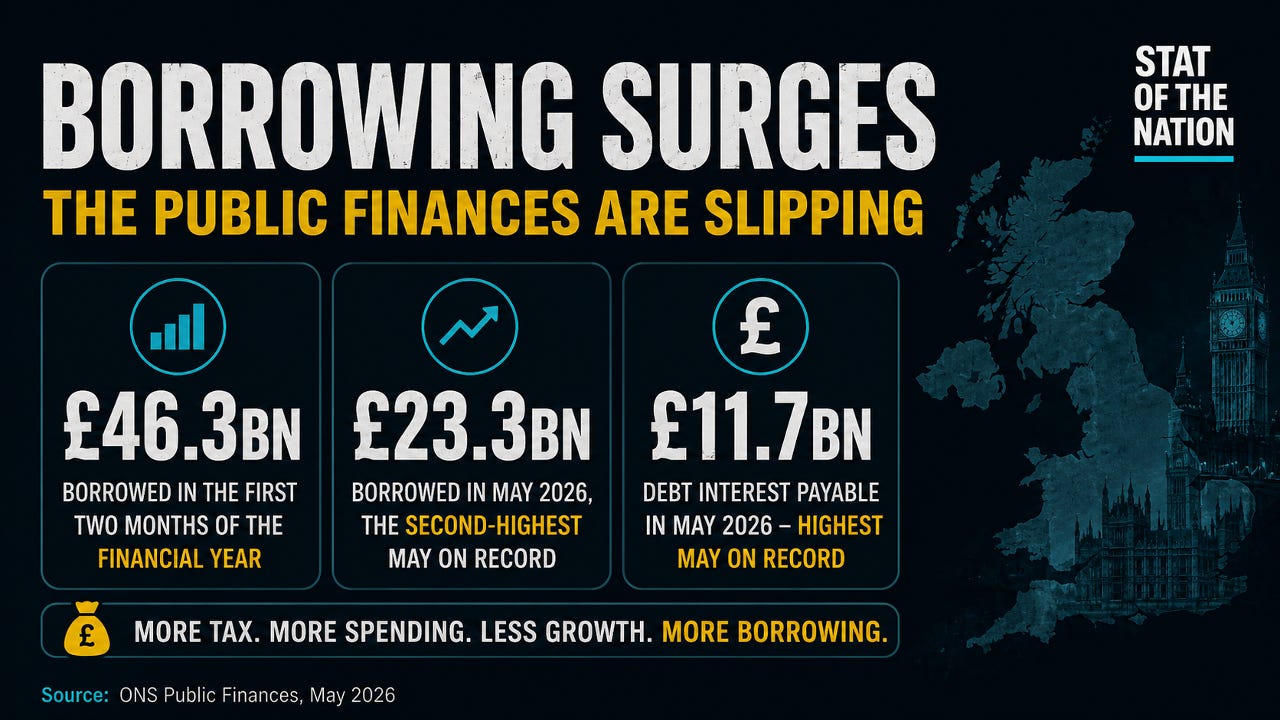

Those figures showed the Treasury had already borrowed £46.3bn in the first two months of the financial year, £7.7bn above the OBR forecast.

In other words, markets were not just looking at who might lead Labour next. They were looking at the numbers any Labour leader would inherit.

And the numbers are ugly.

The Borrowing Numbers Were Already Bad

The UK borrowed £23.3bn in May 2026. That was the second-highest May borrowing figure on record, beaten only by May 2020 during Covid.

It was also:

£5.4bn more than May 2025

£5.6bn above the OBR forecast

Part of a £46.3bn borrowing total in the first two months of the financial year

£8.9bn higher than the same point last year

£7.7bn ahead of the OBR forecast

This is not a minor monthly wobble. It is the public finances running ahead of forecast almost immediately.

The Government is taxing more, borrowing more, and still missing the numbers.

Debt Interest Is Eating The Room

The most alarming figure is not just the borrowing total. It is the cost of servicing the debt.

Debt interest payable by central government hit £11.7bn in May. That was £4.1bn more than May 2025 and the highest May debt interest bill on record.

This is the trap Britain is now in. Years of borrowing have created a situation where a huge chunk of money is spent before any politician has made a new decision. The bills from past choices arrive every month.

That money does not build a new hospital, fix a road, cut waiting lists or improve productivity.

It is the cost of yesterday’s promises.

Labour’s Problem Is Spending

The standard Labour answer is nearly always the same: tax more.

But that argument is wearing thin. Taxes are already high, and yet borrowing is still rising. That tells us something important. The problem is not simply that the state has too little money. The problem is that the state is trying to do too much with an economy that is not growing strongly enough to carry it.

This is why it is hard to believe Labour has the political DNA to control spending. The instinct is always to expand the state, protect programmes, increase benefits, hire more people, and then tell the taxpayer it is all necessary.

But the public sector is funded by the productive economy. If the productive economy weakens while the state expands, the gap is filled by tax rises, borrowing, or both.

That is exactly the loop Britain is now stuck in: more tax, more spending, less growth, more borrowing.

The State Keeps Expanding

The latest public sector employment figures underline the point.

Public sector employment was estimated at 6.19 million in March 2026, up 37,000 on the year. Central government employment hit a record high of 4.07 million, up 46,000 on the year.

The Civil Service employed 558,000 people, up 8,000 on the year. NHS employment was 2.07 million, up 6,000 on the year.

Some of this reflects classification changes and academy conversions, but the broader direction is clear: the central state is larger than ever.

And it is not just the headcount. It is the pay bill.

ONS earnings figures show annual regular pay growth of 5.1% in the public sector compared with 2.9% in the private sector in February to April 2026. ONS notes that public sector pay growth is affected by the timing of pay awards, but the political point remains: the part of the economy funded by taxpayers is seeing stronger pay growth than the private sector expected to fund it.

That does not mean public sector workers do not deserve fair pay. But it does mean the state is expanding while its wage costs are also rising faster than the productive base beneath it.

Every public sector salary, pension contribution, benefit payment and departmental budget line has to be funded from somewhere.

It comes from taxation, borrowing, or both.

The Private Sector Carries The Bill

The private sector pays for the public sector. That should be obvious, but too many politicians talk as if government money appears from nowhere.

It does not.

It comes from workers, businesses, profits, investment, wages and future taxpayers. When the private sector grows, the state can collect more without necessarily raising tax rates. But when private sector confidence weakens, employment softens, business costs rise and investment stalls, the tax base is damaged.

That is why higher taxes can become self-defeating. They may raise money in the short term, but they also risk weakening the very economy the state relies on.

This is the danger of the current model. The Government squeezes businesses and workers, the private sector slows, revenues disappoint, spending keeps rising, and borrowing fills the gap.

That is not a plan.

It is a loop.

Benefits Are The Spending Question Labour Avoids

If Britain is serious about controlling spending, it cannot avoid the benefits bill.

In 2025/26, the Government is forecast to spend £322.6bn on the social security system in Great Britain. That is 10.6% of GDP and almost a quarter of total government spending.

Within that, around £145.0bn is forecast to be spent on working-age and children welfare. That includes Universal Credit and its predecessors, alongside non-DWP welfare spending.

This does not mean cutting support from people who genuinely cannot work. A decent society protects the vulnerable. But a serious country also has to confront the parts of the welfare system that pull people away from work, trap households in dependency, and allow economic inactivity to become permanent.

Too much of modern government spending is not productive. It does not build capacity, raise growth, strengthen the tax base, or help people back into work.

It simply maintains failure.

Politicians love announcing compassionate spending, but they rarely want to talk about whether that spending is producing better outcomes. More money is treated as proof of virtue. Results are treated as optional.

But if spending does not improve productivity, health, work, skills, or economic participation, it eventually becomes another bill handed to the taxpayer.

Burnham Is A Symptom, Not The Disease

This is where Andy Burnham matters.

Burnham has positioned himself as the Labour figure who wants a more interventionist, more state-led, more explicitly left-wing economic offer. He has previously talked about the need to get beyond being “in hock to the bond markets”.

That may sound attractive to parts of the Labour movement. But it sounds very different to the people lending Britain money.

Bond markets are not sentimental. They do not care about slogans. They care whether the sums add up.

The danger is not simply that Labour changes leader. The danger is that Labour changes leader and decides the lesson is not “spend less”, but “spend more loudly”.

If a weakened Starmer is replaced by someone promising more spending, more state intervention, more borrowing, and more protection from hard choices, the market reaction should surprise nobody.

Reeves Is Trapped

Rachel Reeves has spent her time as Chancellor trying to sell herself as the guardian of fiscal discipline.

But that position is now under pressure from both sides.

On one side, the public finances are deteriorating faster than expected. Borrowing is above forecast, debt interest is rising, and the state is still spending beyond its means.

On the other side, Labour’s political mood is shifting. If the party concludes that Starmer is finished, the next leader will almost certainly want a new economic message. And if Labour decides it wants a more left-wing economic offer, Reeves becomes the obstacle, not the solution.

If Starmer falls, Reeves is unlikely to survive the wreckage. Her entire brand is tied to fiscal discipline, but the numbers are already moving against her and Labour’s internal pressure is moving in the opposite direction.

That is why the leadership question matters for markets. A new Prime Minister could mean a new Chancellor, a new fiscal event, a new set of priorities, and a new attempt to persuade voters that Britain can spend its way out of weak growth.

But Britain has already tried too much of that.

Politicians Spend. Taxpayers Inherit.

There is a deeper problem here.

Politicians find it very easy to spend other people’s money. They announce schemes, expand programmes, claim the moral credit, and talk about investment, fairness and compassion.

Then they leave. They resign, get sacked, lose office, move on to speeches, books, directorships, think tanks or retirement.

But the bills remain.

The debt remains. The interest remains. The tax burden remains. The weaker economy remains. And the public is left to pick up the pieces.

That is why borrowing matters. It is not just a line on a spreadsheet. It is deferred taxation. It is a claim on the future. It is money being spent today by people who may not be around when the bill comes due.

The Arithmetic Does Not Change

Labour can change the leader. It can change the Chancellor. It can change the slogan.

But unless it changes the instinct to spend first and ask the taxpayer later, the public finances will keep deteriorating.

Borrowing has surged. Markets are watching. Labour is wobbling. The private sector is being asked to carry a larger state. Debt interest is consuming more of the room. And the benefits bill remains one of the hardest spending questions politicians refuse to face honestly.

So the question is not just whether borrowing has surged.

It has.

The question is whether Labour’s next political turn makes the problem worse.

✍️ Jamie Jenkins

Stats Jamie | Stats, Facts & Opinions

📢 Call to Action

If this helped cut through the noise, share it and subscribe free by entering your email in the box below and get the stats before the spin, straight to your inbox (no algorithms).

📲 Follow me here for more daily updates:

"the public sector is funded by the productive economy. If the productive economy weakens while the state expands, the gap is filled by tax rises, borrowing, or both."

Um, no. Govt's self-funding. Need money? Here's how we get it now; Govt budgets then passes a Supply/Appropriation Bill (look them up in Hansard) forcing the BoE, part of Govt, under the 1866 Exchequer/Audit Act (Google is your friend!) to create, as a loan, the money. Again, Govt is self-funding. It creates money as needed & lends it to itself, daft-sounding I know but here we are. So money for defence, welfare, the NHS, anything productive? Not a problem. Govt, in point of fact, together with its licensed agents the commercial banks, provides the money supply the productive economy needs to function at all. That's the reverse of what you're suggesting here.